Published: Dec 21, 2020

Management:

Wheels India (WIL) is part of the reputed TVS Group… Trust Value Service. TVS Group is a Gold standard for quality of management. Mr. Srivats Ram, MD, WIL, is among the group’s fourth generation leaders.

Summary:

Titan Europe sold its entire shareholding in Wheels India. It could unlock opportunities in new business geographies for the company. I think it is a game changer for WIL.

WIL is trying to diversify its revenue mix and expects to increase the industrial business from 24% to 40%. Margins in industrial space are higher that will improve overall profitability.

WIL is planning to explore more OEMs in wind energy business. Globally, the prospects for wind energy business are looking good. The company has just started exports to one OEM and will explore more OEMs going forward. WIL has emerged as a major supplier to windmill manufacturers in India.

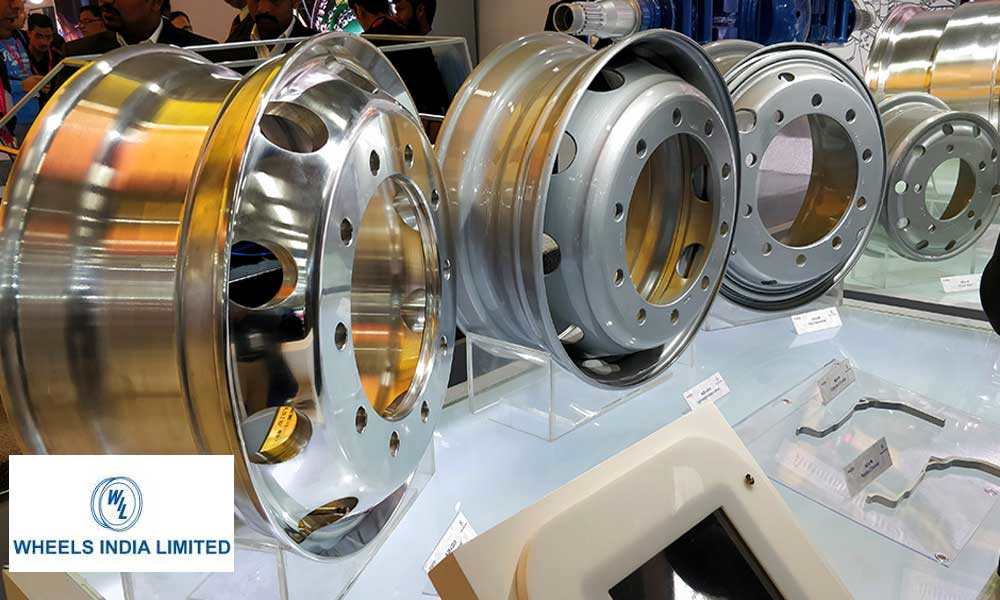

The company has also invested in a ‘cast aluminium wheel‘ factory.

Business:

Wheels India (WIL) is among the largest steel wheel manufacturers in the world. WIL also manufactures air suspension systems for luxury buses and power structures used in the windmill industry. WIL has forayed into manufacturing components for the railway industry.

WIL enjoys sizeable market share – PV (34% share), CV (47% share) and Tractor (58% share).

The current revenue mix of automotive and industrial is at 76:24.

WIL derives 19% of revenue from export market. WIL derives 28% of sales from CV, 21% from PV, 15% from Tractors, 15% from construction and mining, and remaining 21% from air suspension system and other segments.

WIL is focusing on forged aluminium wheel for the CV space.

Capex:

WIL has added considerable capex in 2019 and 2020.

Clients:

Tata Motors, Ashok Leyland, Maruti Suzuki, Hyundai, Ford, Caterpillar, John Deere, New Holland, Komatsu, TAFE, etc.

Dividend:

WIL has consistently paid dividends and the payout ratio is 25%.

Risk:

Any slowdown in the Indian economy will impact its customers adversely.

Penetration of alloy wheels in cars has gone up from 10-40% in the last 10 years. The management believes that the margins and ROI generated from cast aluminium wheels are not attractive.

Investors:

Promoters hold 55.10% of the company

MFs hold 21.59% of the company

Valuation:

Dec 21, 2020:

WIL’s market cap is around ₹ 1130 crore. Historically, WIL has traded in the P/E range of 18 to 25.

At the CMP of ₹ 460, the rate of return is 8.8% based on pre-tax earnings to market cap. WIL is available at .4x times of sales to market cap.

In 2018, 2019, the EPS was around 30. If the EPS returns to 2019-level (pre-COVID), then the P/E will be 16. WIL is trading close to the price that Promoters and MFs paid to Titan Europe.

Oct 4, 2019:

Titan Europe sells 10.4% stake in WIL. WIL was trading at ₹ 600.

June 30, 2020:

Titan Europe sold shares worth ₹ 147 crore in WIL through open market transaction. HDFC MF, IDFC MF and SFH bought shares from Titan Europe at ₹ 427.6 per share.

Oct 30, 2020:

Production commenced at the newly commissioned cast aluminium wheel plant. I think it is a game changer as customers are upgrading to alloy wheels or cast aluminium wheels.

Disclosure:

For educational purposes only.

Leave a comment